MSI Part II - Defence, Management & Strategy, Summary

Part II of my leisurely look under the covers at MS International

After realising my post was getting far too long - it’s now in two parts. Here’s what was in Part 1:

Overview

Background

Current Results

H2 and FY25 estimate

Divisions (excluding Defence)

And now onto Part II where I’ll spend most time on the defence division - 69% of revenue and 86% of profits in the recent interims:

Defence

Some Background

Estimate for H2, FY25 and working capital

Right time, Right Product, Right Place

US Naval Contracts

Land-based Counter-Drone (C-UAV) systems

Service and Support

Tariffs

Management and Strategy

Summary

Before I continue, a reminder: these are my personal opinions. Not advice. You wouldn’t want my advice, I get things wrong. Quite often, more than I’d like, but I’m trying to improve. I’m just a private investor with a fascination for investing in UK small cap companies. I’m biased as I’m a long term investor in MSI and I tend to be too optimistic.

Defence is MSI’s key division, There will be discussion of weapon systems. It’s the primary product of the division and I don’t quite know how to avoid it. I’m not a weapons enthusiast, quite the reverse. Though there is a silver lining. MSI might just be amongst the first weapons suppliers to fail to take lives - and to have saved lives instead - Spoiler - it’s all about defending against drones.

Defence

The part that’s been generating all the interest.

It’s not happened overnight. Many years of patient investment in products and facilities have led to this point. And probably a few setbacks along the way.

By my reckoning the seeds of current success at MSI Defence Systems were sown some 40 years ago.

Some Background

Originally a part of the Norwich based company Laurence, Scott and Electromotors Ltd (an illustrious and innovative company - they made the generators for the Titanic - but perhaps I shouldn’t have mentioned that!) the business has a long history. Over 100 years of supplying the MoD and more recently international customers with its products.

(Source: Google Earth - likely around 2021)

When I’m researching a company - the state of their facilities is always on my list for a snoop. Do the facilities match the image projected by the company? If some of these buildings don’t look like common or garden industrial sheds - that’s because MSI have managed to retain some of the original WWI era Mousehold Heath Aerodrome buildings. Over a century old? But renovated and repurposed very well. I’m impressed? The image is not upto date, further work has been undertaken in the last couple of years in advance of new contracts.

In the late 1980’s MSI management disposed of Laurence, Scott and Electromotors -but retained the defence business eventually renaming it MSI-Defence Systems ltd.

There is one more twist. MSI Defence produced a range of products but I don’t think it made weapon systems until the late 1980’s. When it seems to have acquired the naval anti-aircraft products of the BMARC company, then a UK subsidiary of Oerlikon.

It’s not clear how MSI acquired the products, quite possibly it had been a supplier of key sub-systems. Mounts and fire-control systems being it’s expertise. The rest of BMARC became a part of Astra Holdings which subsequently ‘exploded’ in the 1990’s as a part of the Arms to Iraq scandal - and is written up as a case study in how - not - to make acquisitions. But that’s another story!

MSI’s acquisition has led to greater success than the ill-fated BMARC - now it looks like remarkable foresight on the part of the (then new) management at MSI.

Within a couple of years MSI Defence had established new products with successful sales to the MoD for their weapon systems. These systems and their descendents are now installed across what remains of the RN fleet and over a dozen navies internationally.

MSI now makes, sells, installs and supports a range of naval and land based automated/remote weapon systems.

Automated Weapon System - You What?

Please bear in mind I’m not an expert in weapon systems. This is just my take - as an interested observer - on what MSI does to design and produce automated and/or remote weapon systems.

Sorry I couldn’t resist it. Though things have changed a lot since I used make airfix kits of anti-aircraft guns (I know!).

When you replace the team that used to serve a gun it needs a lot of sensors, actuators, stabilisation, tracking, feed and control systems. And software, evermore software. When you add the ability to detect, identify, and track multiple targets, communications, remote control systems and network interfaces to operate as part of a networked systesm it’s all becoming software based. Even the ammunition may have electronic systems and firmware.

As well as it’s expertise in mounts, sensors and fire-control systems, MSI is a system designer and integrator. Vertical integration gives MSI a lot of flexibility to adapt the system design and make improvements. NB - I don’t have inside knowledge of their design processes - though the speed of design and performance evolution leads me to believe that they are making continuous improvements. A design culture where the aggregation of marginal gains thoughout all parts of the system leads to ‘best in class’ performance.

( Source MSI-Defence )

More Star Wars than Dad’s Army! MSI doesn’t make the cannon. There are now few makers of high performance cannon and many of those trace their design heritage back to the 1920’s and 30’s as with the Bofors 40mm on the kit. The cannon fitted on the LW30M A2 above is the MK44 Bushmaster II 30mm chain gun, An autocannon now made by Northrop Grumman. It’s derived from from the 1970’s Hughes design for the Apache helicopter and is widely used, very reliable, with a reputation for long life and high availability of advanced ammunition types.

The term ‘weapon system’ recognises that rather than being built around the cannon, it’s just one element of an advanced and complex system. MSI’s products are ‘weapon agnostic’ - cannon of different calibres or from different suppliers can be substituted. The system can also mount missiles (MSI Seahawk Sigma) and in principle the cannon could be replaced or redesigned to mount any type of ‘effector’ (a defence industry euphemism for weapon that fires something beam/projectile to disable a target).

I find it hard to put into words how much the design and performance of these modern systems impacts their capability. Here’s a video

- Weapon Stabilisation (German Beer Test)

that I think brings home just how capable these systems are?

Believe it or not - that was the short version. I’ve left out a lot of the nerdy bits. Particularly on the system design trade-offs, continuous improvement and the use of commercially available technology - all of which fascinate me. For more details on the products /and capabilities - and images - visit the company websites:

and

Home Markets and International Diversification

Defence companies selling into international markets can normally rely upon a robust home market for their products. Sadly the UK’s naval fleet has been shrinking rapidly for decades - it;s now just a handful of surface vessels operational at any one time. At the same time the UK moved almost exclusively towards missiles for air defence rather than cannon. Budgets have fallen even faster and by 2012-2014 - MSI’s weapon system orders fell to unpredictable levels as did revenue and profitability.

Those times have never really gone away. The Royal Navy has a centuries old tradition of using weapons from older vessels to equip new ones. Not helped by MSI products being renowned for their reliability and longevity!

But it’s not just MSI’s problem. In the face of the current (2024) defence review - contracts with UK small defence companies are constantly being postponed, paused and delayed by the MoD. The usual story. Pausing a £10m contract is the contractors problem. Pausing a £10B contract is the buyers problem. Not a happy time! As always there are three options. Live with it, change it, or go elsehere.

MSI chose to go international. Responding with long-term investment, the development of new products designed for the international market and increased its international sales efforts. The international defence market is crowded and highly competitive with companies which naturally jealously guard their home market. It’s not an easy strategy for success. I’ve been there. Takes longer than you ever expect. It’s never straight forward and requires constant investment despite frequent set-backs and delays.

By 2020 despite the continuing disruptions there were promising signs of success in international markets, particularly the US. From late 2022 MSI un-characteristically released RNSs for a series of contracts, larger and longer term, which are a step-up for Defence revenues .

Defence FY25 results?

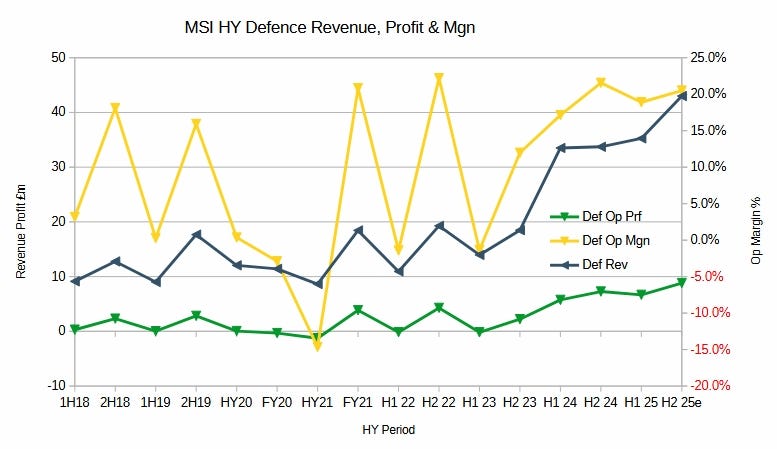

With no forecasts available and very little shareholder engagement - it’s a DIY job and MSI results will be largely determined by revenue recognition at Defence in H2. The chart shows revenue, profit and operating margin at defence for the last 8 years – together with my estimate for 2H25.

The volatility in operating margin reflects the lumpy nature of the contracts and point of delivery - something that MSI has little control over - there are many ways for customers to delay acceptance, delivery and payment - there are few levers for MSI to control which can speed things up.

Revenue recognition is conservative - taking revenue (and profits) only when the product is delivered (when ownership transfers to the customer) and which will depend upon the contract. Prepayments and payments in escrow help to maintain positive cashflow though it causes a build up in contract liabilities.

Many aerospace and defence companies work on contracts with phased milestone payments - I can’t help thinking that as contracts size and duration increase MSI may move in this direction to help reduce the bumps in the road. But I can also see that payment on delivery probably allows MSI more control over its production.

From a low in H1 23 the last few periods have seen a steady increase in revenue - my prediction for H2 is a further increase - based upon what’s been happening with working capital.

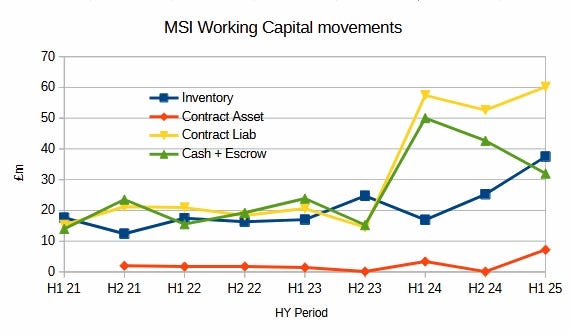

Increased Working Capital

The other divisions only have short term working capital requirements so I’m attributing all the recent increase in working capital to Defence contracts reflecting the work now underway - where revenue and profit have yet to be recognised.

The step change is much more clear in working capital?

It gets quite messy if I attempt to show all elements of working capital - I’ve just charted here the inventory, contract liabilities, assets and the effect upon cash.

H2 Defence estimates

I can’t know what’s happening right now - I estimate H2 figures will be similar to H1 - but with an unwinding of 1/3 of the recent increase in inventory.

I hope this is conservative - as management have said that they expect deliveries to be made over H2 and FY26 and I’m assuming that deliveries expected in H1 were delayed. Not necessarily by much. I’ve made no allowance for unwinding of contract liabilities or contract assets.

Looking at the working capital it seems that there is potential for revenue recognition to be much higher in H2. Though I’d prefer that the numbers were less volatile in future - I’m sure management do too - but we can’t always have what we want. Here’s a part of the chairman’s introduction to the interim results:

Timing of revenue will, therefore, be an increasingly significant feature going forward and, indeed, it has impacted the results for the first half. Nevertheless, the Company is making remarkable advances, even if the half year results do not fully reflect this.

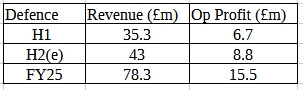

My estimate for H2 (FY25) revenue and operating profit:

What of FY26 and beyond? Will progress continue upwards? Is this as good as it gets? Or will it fade away? To attempt to see what’s likely in future I’m going to look at:

Why MSI products are now in demand - Right Product - Right Place - Right Time

The much larger and long-term US Navy contract,

Land-based systems opportunity,

Support and Services

Right Product - Right Place - Right Time

Very long story - short. It’s all about drones. Or Unmanned Air, Sea and Gound-based systems.

It might surpise you to know that unmanned aircraft have been around as long as aircraft have been used in warfare. Britain flew its first unmanned aerial target in 1917. It’s in the IWM . As it appears to have survived, does that mean we’ve been struggling to counter drones for just as long?

Why are they called drones? Before WWII Britain developed a series of unmanned aerial targets. It’s thought that the use of the term ‘drone’ arose as a name inspired by the DH.82B Queen Bee.

But I digress. Again. Back to the point - but once again - don’t mistake me for an expert. These are just my impressions of MSI’s advantage.

Right Time

The sudden prevelance of low-cost drones in warfare has caught a lot of countries/militaries by surprise. Decades of developing ever higher performing aircraft, and indeed drones, has led to increasingly high performance missile defence systems. Which are way too expensive - upwards of $100,000 a pop for even the cheapest, sometimes over 1$m - and produced slowly in woefully low quantities. Not good enough for defending against drones now often costing $1,000 and downwards. It makes the cannon appear to be a more efficient and more cost effective option particularly against agile swarms of drones.

It’s not just Russia and Ukraine, though that’s where a lot of the rapid development is taking place. Drones are now being widely used (Jordan, Syria, Red Sea, Sudan etc) to attack a range of targets - many of which are not well protected by existing air-defence systems. Unfortunately I can only see the prevalence of drone-attacks increasing. Probably swiftly.

As drone attacks can be launched by just about any military force no matter how small a new and rapidly growing market for defence is emerging. Counter-drone protection of critical infrastructure - eg Energy installations, Communications, Airports, Ports and Shipping - Strategic assets of just about any type. I probably should have said that the market is re-emerging - as defending critical infrastuture with anti-aircraft systems used to be the norm - but seems to have got lost during the during the arms race of the cold war and subequent apparent peace dividend. Oooops! But suddenly it looks like a good time to be the maker of a ‘best in class’ counter-drone cannon system!

Right Product

MSI designed a system that can be installed on small vessels, vehicles or containerised and transported to a location. Which can operate independantly on a stand-alone basis and also has the capability to integrate into defensive networks. Very flexible. It meets the requirements for defending critical assets - at a price allowing suitable quantities to be deployed relatively cheaply in comparison to the value of the assets.

MSI has a first mover advantage - in that it’s product has already been developed and is deployed in service while competitors - and there are many - are playing catch up.

Right Place

Right place - in the market. The protection of critical infrastructure looks to be a rapidly expanding requirement. It’s in this relatively new market counter-drone defence where MSI’s product possibly has the highest future potential and at a price/performance where it is currently a market leader.

There are competitors which offer higher performance - but at a cost that is probably prohibitive for procurement in large numbers (eg Rheinmetall, BAE(Bofors), Nexter). Possibly upto an order of magnitude above MSI and not designed for stand-alone operation.

As a friend of mine in the USAF used to say: In the military - better is the enemy of good enough.

It will take take competitors time to re-engineer and substantially reduce costs. Though I expect they will get there - if the market is large enough and there is nothing like losing a few contracts to concentrate the mind.

There are also competitors offering lower performance at much lower cost. Typically these are smaller mobile weapons and mounts designed to be integrated with a vehicle (Kongsberg, EOS(Australia)). These systems appear cheap but tend to rely upn the vehicle they are mounted upon for a part of their systems. As well as having less capability and performance the systems are not necessarily cheaper once the cost of the vehicle is included.

MSI is one of the few companies that has developed a system that meets the requirements for counter-drone systems with best in class performance, has the option of stand-alone operation and at a better price/performance point and lower through life cost than it’s peers.

It’s also won a major competitive tender for a large long term contract for one of its products the Mark 38 Mod 4 being installed across parts of the US Navy fleet.

US Navy Contracts

It didn’t happen overnight. In the FY24 Interim report the chairman stated: ‘I first reported on our efforts to break into the US Navy market in my Chairman's Statement of 25th July 1988’.

The US DoD has a massive budget. FY25 is authorised at $900Billion. The US Navy operates hundreds of surface ships - and despite well publicised criticisms of its shipbuilding - it commissions more ships every year than the RN has operational.

After the suicide attack on the USS Cole the US Navy determined it lacked defensive weapon against small surface boats and rolled out a weapon system - Mark 38 Mod 2 - based upon a 25mm cannon. United Defense (subsequently acquired by BAE Systems ) won the $395m contract and has been rolling out systems across the USN since 2004. BAE is still rolling out upgrades, the Mark38 mod 3 - 20 years later!

In 2019 the USN undertook a rapid acquisition program to replace the Mark 38 mod 2/3 - for the Mark38 Mod 4 - to provide greater effectiveness for C-UAV/USV with improved accuracy and effectiveness. The system is fully automated and operates remotely on a standalone basis as well as being able to operate as a part of the ship’s Aegis-9 Combat System.

*- C-UAV or Counter Unmanned Aerial Vehicle. C-USV or Counter Unmanned Surface Vehicle

I don’t know how many bids the USN received for the Mark 38 mod 4 tender - but as the incumbent for 20 years BAE Systems was in prime position to win the competition.

To win to against the incumbent supplier - MSI would have had to make no mistakes, offer a better system against the requirements, at a better price and with better customer support. It says a lot for MSI’s product, management and project team that they won the competition.

After supplying 8 systems for trials and evaluation - MSI released RNS statements in late 2023 on receiving first orders for production: $23.5m for mounts (I believe that the cannon is provided directly by Northropp Grumman) and $16m for Electro-Optical sights. Together with a 5 year $50m contract for support services to be provided by MSI-Defence Systems US. (Keen observers have also noted additional small DoD contracts to MSI-Defence US for repairs and test systems for calibration).

The USN plans to roll out the Mark 38 Mod 4 across large parts of its surface fleet starting with the ‘Arleigh Burke’ class guided missile destroyers. The firsr Mark 38 mod 4 systems have already been installed and are in service in late 2024. It might not seem like it - and it doesn’t feel like it - but just 5 years from the start of the acquisition program to the first in service installations is very fast!

MSI should win follow on production orders in the coming months - though comments with its usual caution that it ‘is well placed to win’. For the USN to change horses at this point would be very difficult, expensive and cause a massive delay. But nothing is certain until it’s happened.

It’s now MSI’s contract to lose in future procurement awards. In my mind they do have three advantages for the future:

[1] They got this far without putting a foot wrong - why would they mess it up now?

[2] They are now the incumbent contractor. There is a large cost and resource implication if the USN suddenly decides to switch suppliers - and current production contracts are sole source (ie not competitive tender) under 5 year framework contracts.

and [3] these counter-drone systems have only become more urgent. Despite Trump’s unpredictability counter-drone systems are one of the DoD priorities that is exempt from current cuts.

If MSI can continue to build good relations with their customer and the systems gain a good reputation in-service then there will be many years, decades even of production, support and upgrades. As an established supplier with a good reputation - MSI is well placed to gain further contracts*

*- Back in the day, a quarter century ago, when I was part of a team selling UK systems to NASA and the USAF I was advised to start by signing a contract for a bolt, but always make sure that the Space Shuttle was a contract option - you get the idea?

International Sales

While the Mark 38 Mod 4 is a big step up for MSI Defence I think that value of the contract as an endorsement is just as massive. It’s a big advantage and selling point for other international customers looking to choose between suppliers. It may already be helping customers to come to a decision. And even applying pressure to the UK to turn to MSI for more systems in the future! Highly ironic that it might need international success to stimulate the home market! But it won’t be the first time.

Land-based Systems

Naval systems are MSI’s heritage and new contracts look set to more than double annual revenues going forwards. But it’s a small market in comparison to the market for land-based counter-drone defence systems.

MSI has been working on land-based systems for years but production contracts have eluded them. The market is fiercely competitive with many suppliers defending their position - so gaining access as a new entrant is difficult - and the requirements for remote weapon systems have primarily been for mobile and vehicle mounted systems. Typically much smaller than MSI’s existing Naval systems. I assumed that it would take many years for them to become successful - if they were lucky.

When MSI announced a £22m order for 7 Drops* based (truck transportable) stand-alone counter drone systems in December 2022 - it was a pleasant surprise to find I was wrong. All the more so when that was followed by two orders totaling £54m in 2023 (not RNS’d but revealed in the Annual Report).

* - DROPS - Demountable Rack Offload and Pickup System is a palletised system based upon ISO container mounts and allows transportation by a single military logistics vehicle.

MSI has a ‘first mover advantage’ in the market. Their lightweight naval system designed as a low cost option for small vessels eg patrol boats turns out to be an excellent cost-effective basis for an automated stand-alone land-based system. Particularly for the protection of critical infrastructure.

New Orders?

As the last of the current orders are likely close to being delivered - no large new orders have been announced. MSI are always very frugal with statements and continue to tease us that interest is high and expected to lead to contracts.

To be fair to MSI - defence sales are always like this. There will be NDA’s at least and customers really don’t take to being badgered by suppliers anxious to make PR out of the contract. I’d prefer that MSI focus upon delighting their customers - rather than antagonising them. But all the same - as a new entrant to the market - first mover advantage is notoriously fast to be undercut by competitors with established products. Competition is not only fierce - it’s often not fair. Politics can become a major issue particularly where incumbent and domestic producers are defending their turf.

MSI have recently completed an investment in production facilities capable of the increased production levels that they expect in future. Which gives some indication of their level of confidence. All the same I’d like to see evidence of contracts to show that MSI’s competitive advantage in this land systems market is longer lasting!

Size of the Market

There is an enormous opportunity for MSI in the market for counter-drone systems - specifically in the defence of critical infrastructure - where MSI currently has an advantage.

Even a tiny part of this market would double MSI’s expected revenue of naval systems. Another £50 - £70m revenue annually.

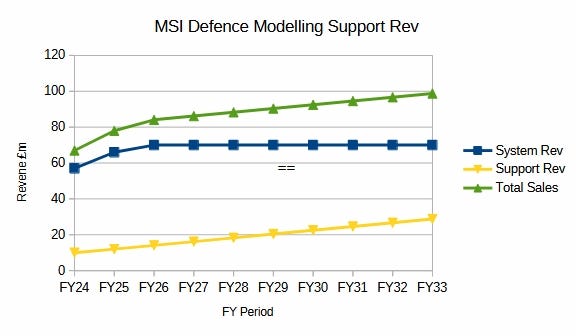

Support Services

There is a third element of the Defence business - customer support. The long term reputation of the company and its products depend upon this. MSI seems to be doing a good job here.

It also represents a valuble base of continuing business which can help to insulate against the variability of short term contracts and lumpy deliveries and provide a rising source of revenue as new systems are installed.

MSI services cover support, spares, maintenance and training. Depending upon the extent of use, and the age of the systems - support services probably - my guesstimate - entail between 2 and 5% annually of the cost of the installed system. MSI also provides repair, refurbishment and upgrades - I’ve no way to know how much revenue this might generate. Probably not likely to be as regular a source of revenue, but every little helps?

I am currently assuming that MSI starts with service and support business currently around £10m annaully. The chart shows the effect upon support revenue increasing at 3% of installed value - each year, with a system sales base flat at £70m annually.

I hope that I’m being reasonable, maybe even conservative, at 3% annually - it serves to show that support services form an increasingly significant part of revenue, even if system sales aren’t growing very fast.

US Tariffs

Not something I thought I’d be considering this time last year. But probably should have been.

Having checked the Federal Acquisition Regulations (FAR 52.229) - My understanding (others may differ) is the US government is obligated to:

Pay/recover any change in import taxes/duties subsequent to the contract signature.

Or provide an certificate of exemption from tariffs whichever is applicable

This applies to systems and components where the US government is the end customer

Which does seem to limit the implications for MSI of the currently imposed tariff regime. Or any regime that might be imposed next week.

With MSI Defence Systems US probably handling an increasing level of the work particularly for customer support, installation and test - there is also another route to minimising the impact of any tariff on the contracts - and maximising the US content of its products is always helpful for winning future contracts in the US.

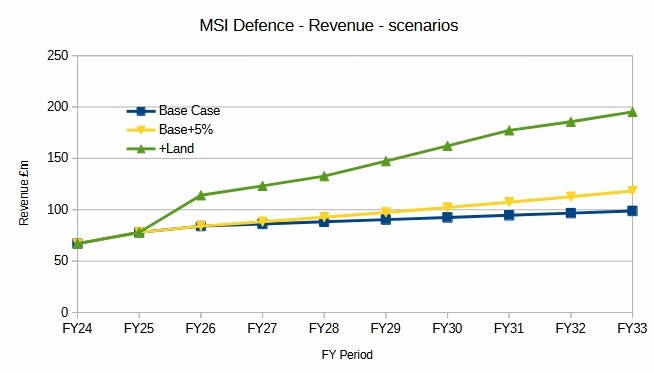

Summary - my view of Defence future prospects

This isn’t meant to be a prediction - just a trend to show where things might end up with

A base case only slightly above FY25 estimate and rising support services,

Annual sales increasing at only 5% and,

With the impact of land-based systems roughly doubling annual system sales

The chart doesn’t cover the full extent of possibilities - just three scenarios that I see as reasonably and relatively likely in a few years time.

The figures are clearly unrealistic - results will be much more volatile based upon lumpy deliveries - I’m intending to show the trend. Resulting in:

A range of revenues from £100m to £200m annually

Likely pre-tax profits in the range £20m - £50m

Long term valuation? Finger in the air range £250m - £750m which reflects the wide range of profits and the wide range of multiples that could apply?

Downside? There is always a downside. In this case I believe its limited with MSI already trading on a low valuation thanks to the lack of forecasts and shareholder communications.

Essentially future success is discounted close to zero at the moment.

Management, Board & Strategy

In recent results management stated

‘Our review of the future strategic priorities of the business is nearly complete’

In the absence of any clarity, in view of the age of the current board, and the recent granting of phantom options (which vest in the event of a change in control of the company) then naturally shareholders speculate on what might be happening.

Speculation ranges from shifting the chairs on the board to allow for succession - through to selling the whole or part of the company.

I see four options:

Selling all or part of the business

Possible bid for defence division

Future succession and strategy

What to do with the cash pile?

Selling up: I’m probably biased but I’ve seen nothing to indicate that management are preparing to sell a part or all of the company.

After spending 40 years getting to this point - why would they sell up now, just when things are getting interesting? Not everyone wants to retire and put their feet up or play golf? By Warren Buffett and Charlie Munger’s example they have some road left to run?

Bid for Defence: There is a real prospect that a multi-national competitor might choose to pay a handsome price for the defence division or less likely the whole company. Sometimes a premium can be paid to take out the competition. Unwanted bids can be distracting for a board. I think it’s likely that the phantom options granted to the NED are in recognition of his role in managing any approach or negotiations.

It’s always better to let bidders approach you than appear keen to sell? If management are not keen to sell - there still may be a price at which they would be willing.

Future Succession and Strategy: Based upon management track record I’d expect them to be working to ensure succession through a capable executive team running the operations - allowing current management to remain as back seat drivers. As a part of this it might make sense to establish a holding company structure. Easing future dispoals or further acquisitions. I could be wrong but I don’t see any indications that management are keen to retire? Any more than they are keen to sell the business?

What to do with the cash-pile? Assuming that success continues in near future the cash-pile will only continue to grow. The choices are: return excess to shareholders through a cash return or buy-backs, or make acquisitions. There have been few signs, as yet, that management is keen is return cash in excess of the dividend or that they are willing to start a large programme of buy-backs.

Acquisitions are expensive in the defence sector right now - though there may suppliers which could add value at a reasonable price. Adding scale to the other three divisions would be a way to speed up their return to growth and acquisitions in these sectors may be better value?

Overall I’d see the most likely strategy as - creating succession with a board capable of running the operations well in the long term alongside a more corporate structure. With one or more acquisitions in the medium term, accompanied by rising dividends and rising shareprice as success is established. A bid is a possibility that can’t be ruled out. Further success may make it more likely - and at a higher price.

Summary

Some of the key points from these two posts:

MSI comprises 4 divisions three of which, forging, superstructures and branding are closely related

The fourth - MSI defence - is historically related but operates completely independantly

Management control the business through their effective shareholding >50%

There are also risks associated with management control. They do not obviously have enough control to delist. And have not been attempting to significantly increase current shareholding.

Owning 50% gives them significant ‘skin-in-the-game’ and substantial alignment with external shareholders despite the lack of shareholder engagement.

Management have invested consistently in all divisions over decades.

Research shows that companies with ‘family/founder’ management tend to perform better in the long run .

Which works well for long term shareholders - perhaps not so well for short term investors?

Prospects for all divisions are good. But timing is uncertain as is the global economic outlook.

Prospects are highest for Defence, though it would be wrong to rule out other divisions also achieving high long term success

Conequently progress at Defence will determine the course of the share price at least in the short to medium term.

Scenarios based upon defence prospects give a range of future valuations from +50% to plus +500% of current market value. Highly dependant upon multiple.

Downside is limited by the pile of cash on the balance sheet, cashflow, dividend and current in-expensive multiple of the share price.

Having invested 40 years in developing the group there is no indication that management is preparing to sell any or all of the divisions.

Probably because selling now is not necessary and fails to achieve optimum value

There is evidence that management are arranging the board to allow them to step back from operations - and focus on the longterm future direction of the group

The growing cash-pile may be utilised for bolt-on acquisitions where they might add significant value to the group.

Phantom options granted are more likely to represent preparations to defend against a bid for the company, or an offer that is hard for management to refuse. Allowing the long standing NED to manage any process without unduly distracting the board from building on current success.

I started out by saying I have no illusions that I can predict the future. I’m very conscious that my posts have dwelt on the upside, not so much on the downside. But that is the way I see it - and maybe I’m wrong here. If I’m wrong then I’m in good company - as the chairman reported in the interim results:

‘I am pleased to report that the good progress continues and I remain even more optimistic about our ongoing performance and prospects than I was at this time last year. ‘

That’s quite an optimistic outlook. This time last year profits had just doubled and the chairman has not been given to over-statement over many years?

Which is why I like it when I’m invested in a company which consistently invests in its own future success, earns a high rate of return on that capital (currently 24.5%), with proven management, has plenty of cash on the balance sheet, pays a solid dividend and not expensive when valued on its current results.

It’s why MSI is currently 45% of my funds. Though admittedly it’s also got something to do with the rest of my investments which are currently not doing as well?

All the remains now is for me to - do nothing! Thank you enormously if you’ve managed to make it this far! Despite the length of these two posts - there was a lot I had to leave out. I value constructive criticism, please leave thoughts and comments - I look forward to reading and replying,

cheers

Mark

A further excellent write up Mark and although the lack of narrative from the Board on contracts etc is frustrating, it is possible to glean some good information from the industry press albeit caution is advised particularly as timescales often seem to slip as you have noted.

I’m looking forward to results (early July I’m expecting) and hope that the H2 out turn translates to Group EPS in excess of 100p (120p+ is feasible) but your cautious approach is to be heeded 👍

Superb write up Mark. I hold MSI but only for the last 3 yrs or so. It is difficult to find information on contracts but as you rightly highlight in defence that goes with the territory. I am very optimistic for the future and the recent management comments give encouragement. I suspect land based could be the jewel in the crown. I personally think within defence sector there must be some competitors having a look and with the profile of the current board and phantom options for the NED it is a real possibility. Also any management options to my knowledge have been taken not even a % sold to cover tax. Look forward to FY25 results.